Best Callable CD Rates on Raisin in July 2025

✓ Federally regulated banks and credit unions.

✓ No fees from Raisin. $1 minimum deposit.

✓ Top interest rates with guaranteed returns during non-call period.

Compare Callable CD Accounts on Raisin

$

Bank

Product

APY

Maturity

mph.bank, a division of Liberty Savings Bank, F.S.B., Member FDIC

Callable CD

4.30%

60 months

$2,150.00

Raisin is not an FDIC-insured bank or NCUA-insured credit union and does not hold any customer funds. FDIC deposit insurance covers the failure of an insured bank and NCUA deposit insurance coverage covers the failure of an insured credit union.

What are callable CDs?

Callable certificates of deposit have been a powerful tool generally used by high-net-worth individuals with financial advisors for years — and are now available to Raisin customers through our no-fee savings marketplace. These CDs offer fixed, premium interest rates for their entire terms, allowing savers to earn some of the best returns possible on deposit products from federally regulated banks and credit unions.

In exchange for these top rates, the bank or credit union offering the callable CD retains the option to “call,” or redeem, the CD prior to its maturity date.

What are the benefits of callable CDs?

Callable CDs offer savers a way to earn a premium interest rate that is guaranteed through the CD's non-call period — with the potential to keep earning that rate for the rest of the term. As with traditional high-yield CDs, callable CDs are generally considered to be low-risk investments.

How callable CDs work

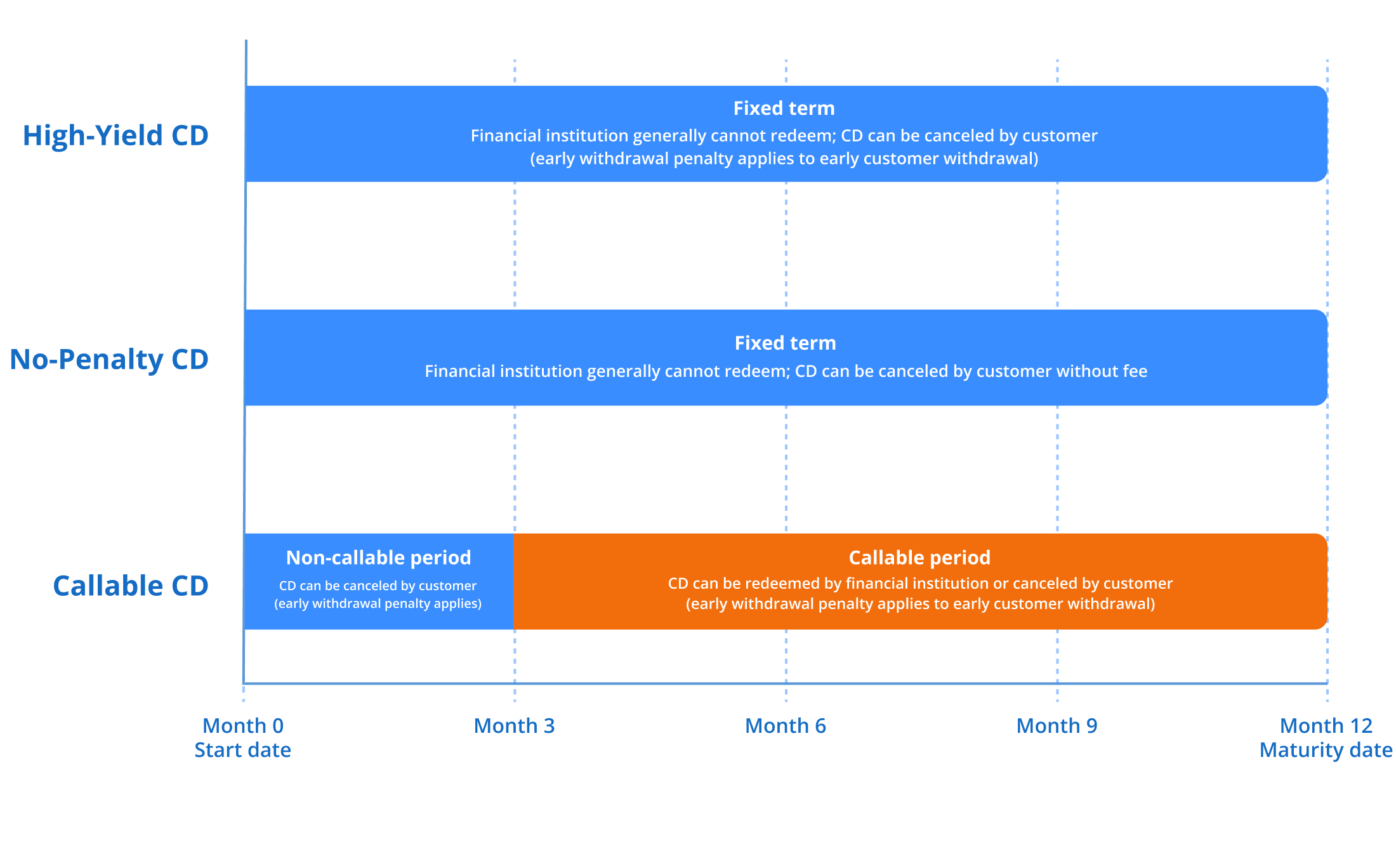

At the start of a callable CD's term, there is a non-callable period during which the CD cannot be redeemed, or "called," by the issuing institution and returns are guaranteed. After this period, the CD continues to accrue interest at the same fixed rate, but with the possibility for the bank or credit union to redeem, or "call," the CD.

In cases where CDs are called prior to maturity, there is no loss to principal or interest accrued up to the call date. In cases where callable CDs are not called prior to maturity, the saver ends up earning that same rate throughout.

Take a look below for an illustrative example comparing 12-month high-yield and no-penalty CDs to a 12-month callable CD with a 3-month non-call period:

Callable CDs vs. High-Yield CDs

Callable CDs | VS. | High-Yield CDs |

Bank or credit union can redeem the CD after the non-call period ends. | VS. | Bank or credit union continues to pay interest until maturity date, even if rates change. |

Deposits earn interest at a fixed interest rate until the CD’s maturity date or the bank or credit union calls the CD. | VS. | Deposits earn interest at a fixed interest rate until the CD’s maturity date. |

Rates are typically higher than high-yield CDs. | VS. | Rates are typically lower than callable CDs, but higher than high-yield savings accounts. |

Higher Interest Rates

Callable CDs can offer higher interest rates than fixed-term CDs or no-penalty CDs, however the issuing bank or credit union can end the deposit prior to maturity.

Fixed Interest Rate

Callable CDs pay a fixed interest rate and have a period of time during which they cannot be called.

No Loss in Principal

If a callable CD is called, there is no loss in principal. All funds, including interest accrued up until the call date, are returned to the depositor.

Frequently asked questions about callable CDs

What is a non-callable CD?

A non-callable certificate of deposit, also known as a high-yield CD or fixed-term CD, is a type of account offered by banks and credit unions that allows you to deposit a set amount of money and commit to leaving it there for a fixed period of time, known as the CD term. In exchange, you earn a fixed interest rate for the deposit’s entire term, allowing you to more accurately predict your returns than funds held in a high-yield savings account, where rates can change over time.

Terms on non-callable CDs can vary from as little as one month to as long as five years (60 months) or even longer.

If my CD is called by the issuing bank or credit union will I be subject to early withdrawal penalties?

If the bank or credit union that issued your callable CD calls it prior to maturity, there are no early withdrawal penalties applied. You would receive back your entire balance, including all interest accrued until the call date.

In cases where you decide to cancel your callable CD prior to maturity, whether during the non-call or callable periods, you would be subject to early withdrawal penalties based on the terms of your specific product.

What happens if I cancel my callable CD?

In cases where you decide to cancel your callable CD prior to maturity, whether during the non-call period or callable period, you would be subject to early withdrawal penalties based on the terms of your specific product.

Are callable CDs worth it?

Because callable CDs may offer higher interest rates than fixed-term CDs, they may appeal to savers that are looking for top rates upfront but aren’t concerned about long-term returns. Even with the risk of the CD being called early, callable CDs typically are considered a low-risk investment option.

If a CD is called early, you will still receive your earned interest and aren’t at risk of losing your principal.

One potential risk of depositing funds in a callable CD is your reinvestment risk. If a bank or credit union calls the CD, it typically means that interest rates have dropped. When you go to find other savings products for your returned funds, you may find less favorable rates available on similar products.

What are a callable CD’s non-call period and callable date?

While callable CDs can be called prior to maturity, banks or credit unions that issue callable CDs typically will have a callable date and a non-call period. The callable date is the date before which a bank or credit union cannot call the CD. The period between the callable CD’s opening and the callable date is known as the non-call period.

What are the risks of callable CDs?

Generally, callable CDs are considered a safe investment option with a guaranteed return during the non-call period.

As with high-yield CDs, funds in a callable CD are typically not accessible prior to the maturity date without paying an early withdrawal penalty. Additionally, while there is no loss to principal or accrued interest in cases where callable CDs are called by the issuing bank or credit union prior to maturity, there is a loss of potential returns between the call date and the maturity date. There may also be a reinvestment risk in cases where interest rates have dropped.

What happens if your CD is called?

If the bank or credit union that issued your callable CD calls it, you receive back your initial deposit (also known as the principal) as well as all interest accrued up to, and including, the day it was called.

Once a CD is called, you forfeit any potential interest that would have been earned if the CD had matured.

How often are callable CDs called?

Banks or credit unions will typically call a CD if interest rates drop — if the interest rate environment changes and they are now able to issue CDs at significantly lower rates, it may no longer make sense to pay the higher rate they had previously offered on a callable CD. Because of this risk, interest rates on callable CDs tend to be higher than those on non-callable CDs.

What is Raisin?

With Raisin, you can access an exclusive network of banks and credit unions offering top rates on no-fee savings products. Find, fund, and manage high-yield savings accounts, money market deposit accounts, and CDs from multiple institutions, all from a single login.

Safety

Raisin partners exclusively with federally regulated institutions with comprehensive cybersecurity programs. Raisin itself invests in a suite of state-of-the-art cybersecurity measures including certifications and assessments, data monitoring and data encryption.

Choice

Choose from a diverse selection of savings products offering flexible terms and some of the most competitive interest rates. You can easily find the right product or mix of products for you.

Convenience

One login to hold all your deposit products. Simplified statements. Easy access to manage your funds – all through a streamlined digital platform.

Security Is Our Top Priority

Raisin is focused on cybersecurity

At Raisin, we invest in a variety of technologies to protect our customer’s data, privacy and transactions. These include multi-factor authentication, encryption, and web application firewall advanced internet protection technologies. Raisin is a SOC 2 certified organization, which means we have met the requirements outlined by the American Institute of Certified Public Accountants (AICPA) to ensure that we have the controls in place to keep customers data secure and private.

Open an Account in Minutes

Select

the right product for your savings goals.

Register

with an email address and password, then verify your identity and bank information.

Fund

the savings products you add to your new Raisin login.

How Raisin Compares

With Raisin | VS. | With traditional banking |

One secure login guards your personal data and safely allows you to tap into yields from multiple savings products. | VS. | Multiple signups, savings accounts, and products at different institutions each require you to provide sensitive personal information. |

The platform brings together diverse and competitive savings products, including CDs with a range of terms, that increase your earnings potential. | VS. | There are fewer product options, possibly limiting your savings potential. |

Only one login is required. You manage all your chosen savings products through the Raisin platform. | VS. | By opening new accounts at multiple institutions, you get more statements, must remember more passwords, and waste time. |

FAQs

Raisin is a free digital platform that gives savers unparalleled access to a variety of deposit products through the convenience of a single login, helping you unlock the growth potential of your cash savings.

With the Raisin platform, you can fund deposit products offered by federally regulated banks and credit unions with a wide range of maturities and APYs (annual percentage yield), allowing you to build a savings strategy to suit your earning and liquidity needs.

Raisin is not a bank or credit union. It provides the digital “storefront” where banks and credit unions can promote their deposit products.

Raisin is operated by Raisin Solutions US LLC, a 100% subsidiary of Raisin SE, a trailblazer for open banking in the deposits and investments space. In the U.S., Raisin helps banks and credit unions improve their deposit funding by offering national reach for their retail deposit products, and provides savers with better access, more choice and higher convenience when evaluating savings products from federally regulated banks and credit unions.

- High-yield Savings Account (HYSA). As its name indicates, this account type functions like a traditional savings account—with typically no restrictions on depositing and withdrawing funds—but earns interest at rates that are higher than the national average for standard savings accounts.

- Money Market Deposit Account (MMDA). Also known as a money market account or MMA, this type of savings account offers a varying rate that allows you to earn interest on your funds with maximum flexibility for withdrawals. Like a HYSA, an MMDA offers features of a traditional savings account with typically higher returns.

- No Penalty CD. Through the flexibility of a No Penalty CD, you can lock in a competitive rate for a fixed term with the option to make a full withdrawal without having to pay a penalty for the early termination. Terms and conditions may vary by product. Please see specific product terms for more details.

- Fixed Term CD. With this longstanding savings vehicle, funds are held for a fixed term, and a competitive interest rate provides safe, predictable earnings. In contrast to No Penalty CDs, typically you are charged a fee if you do not complete the full term of the Fixed Term CD.

Interest (or dividend in the case of credit union savings products) is compounded daily and posted to your account monthly.

At Raisin, cybersecurity is our priority. Raisin is a SOC 2 certified platform, meaning it has been validated by outside auditors across five (5) key information security principles. We also use a variety of measures to protect our customers' data, privacy and transactions, including:

- User authentication. The Raisin platform uses multi-factor authentication combined with leading authentication technology to validate our customers’ identities.

- Data encryption. Your personal information is encrypted in-transit and at rest using advanced cryptographic security algorithms.

- Site protection. Web application firewall advanced internet protection technologies are implemented to protect Raisin.com from malicious actors, botnets and denial of service attacks (DDOS).

- Monitoring. An always-on information security monitoring platform detects and alerts us to information security events.

- Assessments. Our platform undergoes vigorous security assessments and testing throughout the lifecycle of application development, from architecture planning to production phases.

Creating a Raisin login is easy, requires no credit check, and typically takes less than five minutes. Here’s how:

- View the offers on our savings marketplace and select a savings product offered by one of our partner banks and credit unions.

- Follow prompts to enter your email and create a password.

- Complete a simple online application and, after successful identity verification, link a bank account from which to fund your first deposit.

- Start earning interest as soon as your money is received by the bank or credit union offering the savings product you selected.

Any questions or concerns? Email us at support.us@raisin.com.

All deposits and withdrawals are completed within one to three (1-3) business days. After the initial deposit a withdrawals limitation for the first few business days may exist.

Business days are Monday through Friday excluding U.S. bank holidays.

For products offered by banks, all necessary registration is handled when you become a Raisin customer. One of the many benefits of our platform is that you can open a single account and earn competitive interest rates from banks in the Raisin network. When you select and fund a savings product offered by a credit union, there is an additional step of becoming a member. Raisin makes that process quick, easy and free. You still have one Raisin login and can view all your savings products in one convenient dashboard.

The current APY for your savings products can always be viewed on the Account Overview page when you are logged in to Raisin. This information also appears on monthly statements.

You cannot currently link your Raisin login to a third-party app, but we may offer this feature in the future. For now, you will not be able to link your selected savings product to a third-party app even if the bank or credit union offering that product does so outside of the Raisin platform.